Square, Inc.: Financing a Unicorn - Case Solution

This Square, Inc.: Financing a Unicorn case study focuses on the structure of the venture capital private equity funds, the characteristics of internet-based companies and the returns investors would be entitled to in the event of the venture going public or going for a non-public sale based on the terms of their entry.

Case questions answered:

- How are venture capital private equity funds structured? How are private equity firms compensated? Why may Khosla Ventures be motivated to push for Square Inc. to seek an exit?

- What characteristics do the firms in case Exhibit 2 have in common? Do you agree with Marc Andreesen’s thoughts regarding unicorn valuation levels?

- What would the capitalization table look like after the Series E issuance? What is the post-money valuation?

- What returns would each class of investors realize if Square exited through an IPO (rather than through a sale) at valuations of $3 billion, $6 billion, or $9 billion?

- How would the returns change under $3 billion, $6 billion, or $9 billion valuations, if the Series E securities did not have the IPO ratchet? Do you recommend investing in the series E preferred round?

- How are VC funds structured?

- How are PE firms compensated and does it impact the firm’s IPO exit?

- Do you agree with Marc Andressen’s unicorn valuation assessments?

- Construct a cap table after the series E issuance.

- What returns would investors realize if Square had a sale at $3, $6, or $9 billion instead of an IPO?

- Would you invest in a Series E issuance?

Square, Inc.: Financing a Unicorn Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

You will receive access to two case study solutions! The second is not yet visible in the preview.

I. Introduction - Square, Inc.: Financing a Unicorn

This report on Square, Inc.: Financing a Unicorn case study discusses the structure of the venture capital private equity funds, the characteristics of internet-based companies and the returns investors would be entitled to in the event of the venture going public or going for a non-public sale based on the terms of their entry.

II. Structure of the venture capital private equity fund

Venture capital private equities are structured in a way that the firm looking for financial backing (general partner) actively involves investors in supplying capital needs to a fund to keep the business running. Investors hold a role as a provider of capital. They are referred to as limited partners, which usually consist of high-net-worth individuals or financial institutions like banks and insurance organizations (Herciu, 2017).

In the process, a percentage of equity is granted to the limited partners in proportion to their injected capital. Private equity firms get paid in two main ways: management fees for managing the fund, which are paid regularly by the limited partners to the fund, and a percentage of the profits that the fund gains from the investment capital gains called carried interest.

III. Khosla Ventures Pushes for an Exit of Square Inc.

The reason Khosla is eager for an exit is to receive a generous amount of proceeds from liquidation if the exit is successfully executed at current valuations of $6 billion.

Khosla Ventures were the lead investors in the Series A investment, where they bought preferred shares at $0.217. Considering Square’s current planned per share sale price of $15.46, an exit from this investment will realize a return of 3475%.

Square Inc. is faced with issues like an excessive cash burn rate and new entrants in the e-payment market who offer the same service at a lower cost. These issues led Khosla’s management to view Square’s growth in the future as doubtful.

A combination of a high cash burn rate, high valuation, and a disappearing IPO market could lead to a valuation trap that makes the business unsustainable and find it difficult to convince new investors.

IV. Unicorn Firms and a Probable Bubble

Square is considered a unicorn, companies whose post-money valuations exceed $1 billion. By mid-2014, the world saw more than 62 unicorn-level companies globally. A few common traits among all these companies are that they were internet-based companies.

It means their biggest source of revenue was reliant on the internet (Berkman, 2020), and the majority of them were concentrated in the regions where the GDP was high, and start-up culture was a trend.

The combination of similar revenue sources and sky-high valuations led investors to believe the world was headed towards another dot.com bubble-type bearish market. However, Marc Andreesen states that the times were different.

Not everyone in the ’90s had access to the internet, which also meant that the products these companies came up with were not globally accessible, thereby shrinking the target market (Smith, 2020). However, the “.com” companies then were viewed as revolutionary companies, and investors rushed to invest in them as they fed off each other’s hype, creating bubbles in the market (McCullough, 2020).

The highly improved internet speed and the availability of cloud computing and data science made information transfer/sharing and the global distribution of software widely available from 2009-2014, compared to just the dialed-up internet connection in the late ’90s.

The advancement in internet capabilities, accessibility of centralized storage, as well as the massive amount of data available, allowed developers to create algorithms that help the software adapt and tailor to the user’s needs.

Marc Andreesen’s statements regarding “investors anticipating another dot com bubble” are therefore accurate, stating that the ideas of the “.com” companies were good. Still, the availability of resources was not in their favor, and they were ahead of their time.

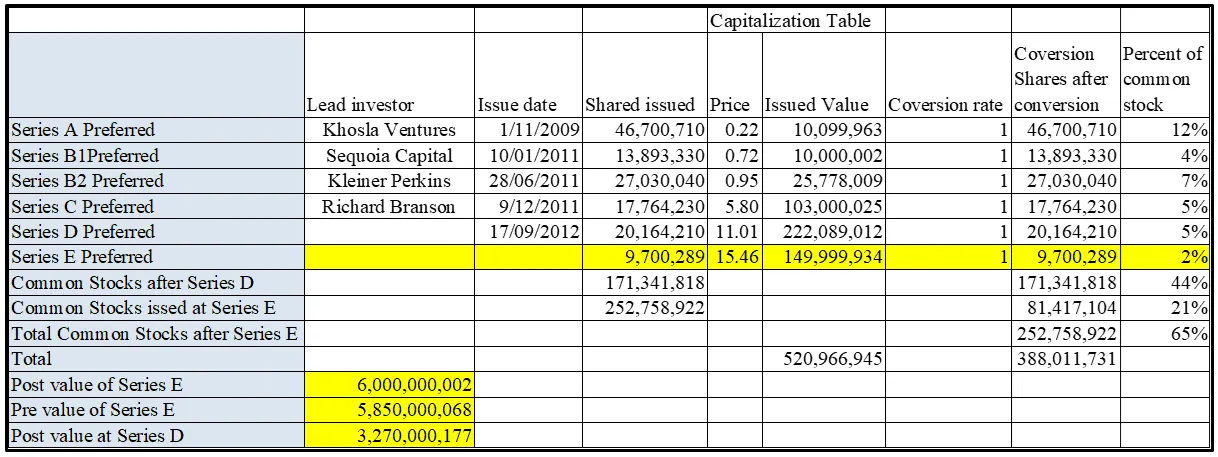

V. Series E Issuance

Appendix 1 shows the post-money valuation of Square Inc. after Series E investments. Post valuation after Series E equals $6 billion and calculated using the following formula: Post-value = Total conversion shares after conversion * Price at Series E

Appendix 1: Post-money Value after Series E

With this valuation, it means that the pre-value of Series E (5,850,000,068) is higher than the post value at Series D of 3,270,000,177.

The value-added might be derived from future expectations of the high growth rate of the firm’s gross payment volume (GPV) and addressable market size. GPV increased by 125% in 2013, and 40.3% in 2014.

Using the average GPV growth rate of 83.82%, Square Inc.’s future market share (GPV/ Credit Card Transaction Volume), and outlook for mobile POS payments are…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.