Spyder Active Sports--2004 - Case Solution

Spyder Active Sports by Spyder Inc., founded by David Jacobs, manufactures and markets advanced ski equipment for professional skiers. He successfully operates the company establishing a major international brand, and has achieved considerable development over 26 years of operation. Would Jacobs’s decision affect the total percentage of shares for sale and the valuation of Spyder Active Sports?

Case questions answered:

- How would David Jacobs’s decision affect the total percentage of shares for sale? Would it affect the valuation of Spyder Active Sports? Why or why not?

- The potential buyer can be publicly traded or privately held, and it can come from the same industry (i.e., strategic buyer) or be a financial institution (i.e., financial buyer). Would the valuation of Spider change depending on buyer type? Why or why not? Explain qualitatively.

- Estimate the value of Spyder using DCF based on forecasts provided by the case. How would your valuation change, depending on the type of buyer (public or private, strategic or financial)?

- Estimate the value of Spyder using market multiples provided by the case. Explain your choice of comparable companies and multiples. Would your valuation change depending on the buyer type (public or private, strategic or financial)?

- What choices does David Jacobs have, and how would his decisions (sell or not to sell, and to whom he sells his shares) affect the valuation? What would you recommend him to do?

Spyder Active Sports--2004 Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

Executive Summary - Spyder Active Sports

Spyder Active Sports by Spyder Inc., founded by David Jacobs, manufactures and markets advanced ski equipment for professional skiers. He successfully operates the company, establishing a major international brand, and has achieved considerable development over 26 years of operation.

One of the partners who owned Spyder is CHB Capital, a private equity firm focusing on building good relationships with companies, like providing useful strategic and operational knowledge to boost revenues together. It is unlike other traditional private companies that buy the company directly.

Another partner, David Jacobs, is also considering selling the company to retire. The company has been using discounted cash flow and multiple approaches for valuation.

Jacob’s decision on whether to sell the company does matter to the valuation of the firm. The feasible way is to sell Jacob’s own equity stake and CHB’s to either a strategic or financial buyer.

Otherwise, Jacob will have to adjust its valuation to receive a minority discount if Jacob decides not to sell. From a financial point of view, since the company is in a period of high growth and the stock market is favorable, it is a good time to sell Spyder Inc.

However, David is also affected by other non-finance factors, which increases the complexity of making decisions.

Exit Options and Considerations

There will be a significant difference among the firms with a different total percentage of shares for sale.

For example, if you acquire more than 50 percent of the equity of a company, you will have larger or absolute control over the company compared to acquiring 49 percent of the equity of the company.

Thus, the maximum price you are willing to pay reflects the optimal value of the firm and your confidence in making more profits for the firm in the future. In this case, there are some different situations.

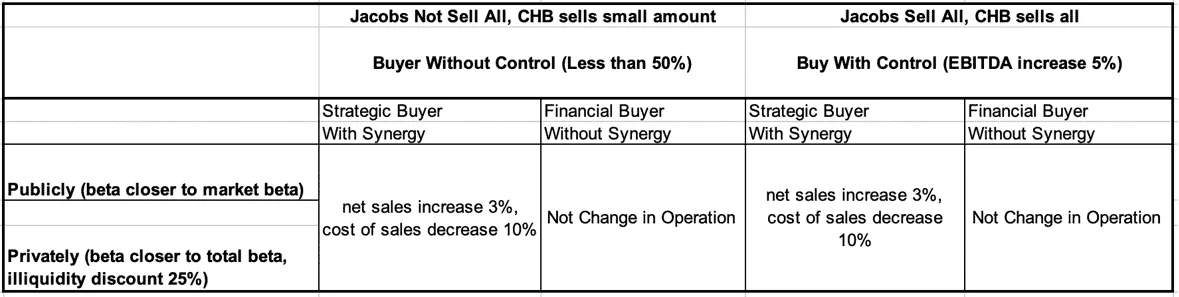

Firstly, if Jacob and Shimokubo sell all shares (12.1%), and CHB sells all shares (37.9%), the total percentage of shares for sale is more than 50%. Thus, the buyer should pay more than 50 percent of the valuation of SPyder Inc., and the buyer will have absolute control of the firm.

Secondly, if CHB provides some of its shares while Jacob and Shimokubo decide not to sell all, it indicates that the total percentage of the shares for sale is less than 50 percent. Thus, investors will not have control of the firm.

Valuation of Spider changes depending on buyer type

On the one hand, the difference between private and public trade is that the buyer is usually not diversified, and the investment is illiquid in a privately held case. In contrast, the buyer is usually diversified in a publicly traded case. Thus, we could determine the value of the firm by using different betas.

To be more specific, we decided to value the firm by using the beta, which is closer to the market beta, to sell to a publicly traded firm, and value a firm by using the beta, which is closer to the total beta with an illiquidity discount at 25% to sell to a privately held company.

Next, we could obtain two different WACC to calculate the different values for Spyder Inc. On the other hand, we determined that the financial buyer and strategic buyer would make the firm value different.

For instance, when a financial buyer purchases more than 50 percent of equity, it can obtain control of the firm, and there will be no change in its operating income.

When the buyer is a strategic buyer with synergy, the company can obtain the value of synergy, and the net sales of the firm will increase by 3 percent, but the cost of sales will decrease by 10 percent.

It also has the control of the firm if buyers purchase more than 50 percent of equity. In addition, when the Financial and strategic buyers purchase less than 50 percent of equity, they also have two situations, as we mentioned above.

Based on the information given above, we got 8 different scenarios, as shown in Table 1.

Table 1: 8 Different Scenarios

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.