Software Associates - Case Solution

Richard Norton, CEO of Software Associates, after going through the profit and loss statement of the last quarter, asked Susan Jenkins, CFO of the company, to explain the deviation why their profit had taken a hit despite exceeding billed hours and revenue estimates.

Case questions answered:

- Prepare a variance analysis report based on the information in Exhibit 1. Would this be sufficient to explain the profit shortfall to the Software Associates CEO at the 8 AM meeting?

- Prepare a variance analysis report based on the information in Exhibit 2.

- Prepare a spending and volume variance analysis of operating expenses based on the additional information supplied in Exhibit 3.

- Prepare an analysis of the revenue change, separating the volume effect (increase in the number of consultants) from the productivity effect (billing percentage).

- Prepare an analysis of actual versus budgeted revenues, consultant expenses, and margins using the additional information supplied in Exhibit 5.

Software Associates Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

From: Richard Norton, CEO of Software Associates

To: Susan Jenkins, CFO of Software Associates

Primary question posed by Richard Norton to Susan Jenkins

Richard Norton, CEO of Software Associates, went through the profit and loss statement for the last quarter. He was glad that they had exceeded billed hours and revenue estimates.

However, their profit had taken a hit. It was half of what they had expected (budgeted). He wanted Susan to explain this deviation.

Software Associates

Software Associates performed system integration projects for clients. Their annual revenues exceeded USD 12 million, and the profit margin was between 15% and 20%. They provided two services,

- Contract

- Solution

The budget

The budget for three months usually consists of 3 main components - consultant revenues, consultant expenses, and operating expenses.

Consulting revenues = number of consultants x number of hours available per consultant x Expected billing percentage x the average hourly billing rate

where expected billing percentage = hours billed/total hours available

Expenses

Operating expenses have both variable and fixed components. Variable components depend on the number of consultants. Occupancy expenses were fixed. Computing and telecommunication had both fixed and variable components.

Revenue problem

The actual number of consultants was nearly 8% higher than budgeted consultants. But revenues had increased by only 1%. Susan set out to find the reason behind this.

Lines of business

The two lines of business had quite different operating characteristics. So, Susan decided to separately account for these two businesses and tabulated the data.

She also wanted to do some additional analysis to find out whether actually Software Associates is increasing or decreasing its share of the consulting business.

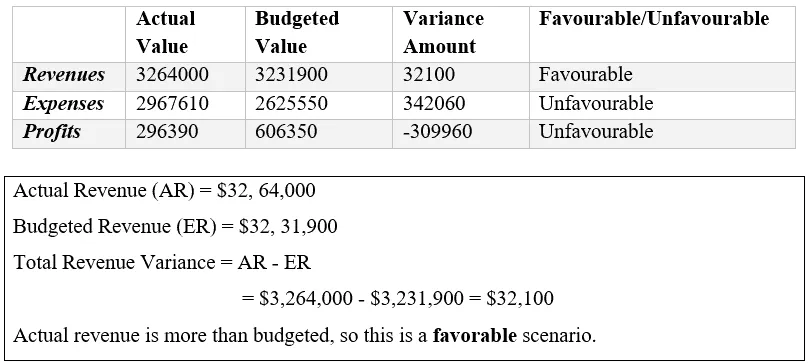

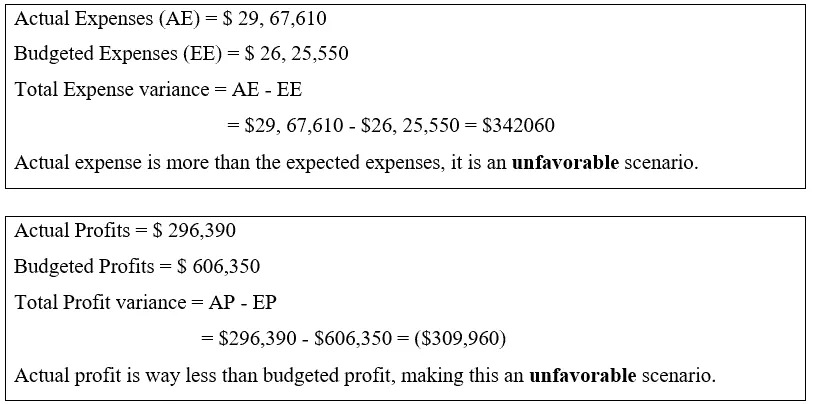

Assignment Question 1

Prepare a variance analysis report based on the information in Exhibit 1. Would this be sufficient to explain the profit shortfall to Norton at the 8 AM meeting?

Analysis:

With the data that has been given in Exhibit 1, we do not have the actual split-up of expenses nor further details about how the two divisions have spent and earned their money. So, the given data alone is not sufficient to find the area of issue.

From the data in Exhibit 1, we can tell that there is an increase in the expense of Software Associates, but we cannot explain why the expense has increased. This gives us a…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.