Seagate Technology Buyout - Case Solution

This Seagate Technology Buyout case study shows the structure of the two-step leveraged buyout transaction carried out by Seagate, Silver Lake Partner LP, and VERITAS. The report contains a detailed analysis of the need for an LBO, the structure and the deal, and the future cash flows of the resulting firm.

Case questions answered:

- Why is Seagate Technology undertaking this transaction? Is it necessary to divest the Veritas shares in a separate transaction?

- What are the benefits of LBO? Is the rigid disk drive industry conducive to a leveraged buyout?

- Luczo and the buyout team plan to finance their acquisition of Seagate’s operating assets using a combination of debt and equity. How much debt would you recommend that they use? Explain why?

- Based on the scenarios presented in Exhibit 8 and on your assessment of the optimal amount of debt used in Seagate’s capital structure, how much are Seagate’s operating assets? Assume that of the $800 million in cash that the buyout team will acquire as part of the transaction, %500 million is required for net working capital and $300 million in excess cash. Assume that the buyout team plans to maintain its debt at a constant percent of the firm’s market value.

- Based on the scenarios presented in Exhibit 8 and on your assessment of the optimal amount of debt used in Seagate’s capital structure, how much are Seagate’s operating assets? Assume that of the $800 million in cash that the buyout team will acquire as part of the transaction, %500 million is required for net working capital and $300 million in excess cash. Assume that the buyout team plans to pay down its debt as cashflows permit until a terminal debt level of 700m is reached.

Seagate Technology Buyout Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

I. Introduction - Seagate Technology Buyout

This Seagate Technology Buyout report shows the structure of the two-step leveraged buyout transaction carried out by Seagate, Silver Lake Partner LP, and VERITAS.

The report contains a detailed analysis of the need for an LBO, the structure and the deal, and the future cash flows of the resulting firm.

II. Reasons for an LBO and divesting VERITAS' shares

The reason for this transaction’s necessity comes from the aftermath of Seagate’s decision to trade their Network & Storage Management Group (NSMG) for 40% (155 million) shares of VERITAS stock, making them the largest stockholder in the company. Six months after the transaction, there is a 200% increase in Veritas’ stock price, compared to Seagate’s “only” 25% increase.

The board of Seagate sensed the firm’s undervaluation despite its large market capitalization and its position as the market leader. It has also become difficult for shareholders to offer stock compensation to managers when the stock performance is tied to Veritas’ stock instead of the performance of the business.

The sale of Seagate’s holdings in Veritas will lead to double taxing if sold within a year of the purchase date. Its prior agreement with Veritas, Silver Lake Groups, and Stephen Luczo, CEO of Seagate, generated an idea to execute a leveraged buyout (LBO), which later on formed as a new company, Suez Acquisition Company (Suez). Silver Lake Group will control the new company.

The process of divesting Veritas shares in a separate transaction was proved necessary as the separate transaction resulted in no immediate corporate or personal tax liability since this merger is considered as reorganization (no gain recognized) under Section 368(a) of the Internal Revenue Code.

Seagate’s shareholders will only be taxed on the portion of the cash received. At the same time, Veritas can “repurchase” its 128 million shares for only 109 million shares while also obtaining Seagate Technology’s high cash balance and additional goodwill from the M&A.

III. Benefits of an LBO

When a firm utilizes a high level of debt to acquire a company, it is classified as a leveraged buyout. The value created from LBOs is often attributed to the availability of ample lower-cost credit, the PE firm’s engineering capabilities, and the improved alignment of interest of management and shareholders (CFA Institute, 2020).

Empirical evidence suggests that price and EPS increases from alternatives like stock buybacks are only short-term because the increase cannot be attributed to organic growth (“Share Buyback- Methods,” 2020).

Similarly, studies conducted by Oppenheimer and Co indicate that a tax-free spin-off that results in the disk drive industry becoming an entity on its own as a Seagate subsidiary states that increases are not sustained (“Spin-Offs - benefits,” 2020). Spin-offs help the company focus on the disk drive business resources to build on long-term growth.

However, it causes the spun-off shares to be even more undervalued in a weak market (like the present), and the Veritas shares still cannot be sold due to the Veritas agreement (Fontinelle, 2020).

Selling Seagate as a whole would mean preceding its future high growth opportunities in data storage and consumer electronic applications while incurring high liquidation taxes (Willens, 2010).

An LBO values Seagate Technology at its fair market value in an undervalued tech market. With Silver Lake’s expertise in tech and its reputation (Serwer & Key, 1999), Suez can obtain more favorable credit terms to lower the cost of capital for future debt loans.

The complete transaction separates the performance of Seagate’s and Veritas’ stock with the business, which helps the new entity to offer stock compensation to management in the future when it is publicly traded again under Suez, which aligns management interest with shareholders.

The disk drive industry is characterized by intense competition with its short product cycle and a limited number of customers while also heavily driven by research and development. These factors increase the uncertainty of the cash flows of the firms in the industry. They also reduce the conduciveness of PE firms to invest in the industry.

However, Seagate’s plan to venture into network data storage and high-margin segments improves its cash flow prospects, and its vertical integration helps it manage consumer demand shifts better than its competitors.

Cheaper financing from an LBO and improved future cash flow are expected to offset higher fixed costs like R&D expenses and expansion capex that help Seagate maintain its position as the market leader. On top of that, Seagate’s shareholders are compensated with a fair market price by selling to Silver Lake.

IV. Buyouts in the Disk Drive industry

The disk drive industry is characterized by intense competition with its short product cycle and a limited number of customers while also heavily driven by research and development. These factors increase the uncertainty of the cash flows of the firms and reduce the conduciveness of PE firms to invest in the industry.

However, Seagate Technology’s plan to venture into network data storage and high-margin segments improves its cash flow prospects, and its full vertical integration helps it manage consumer demand shifts better than its competitors.

Cheaper financing from an LBO and improved future cash flow are expected to offset higher fixed costs like R&D expenses and expansion capex that help Seagate maintain its position as the market leader.

On top of that, Seagate’s shareholders are compensated with a fair market price by selling to Silver Lake.

V. The structure of the deal

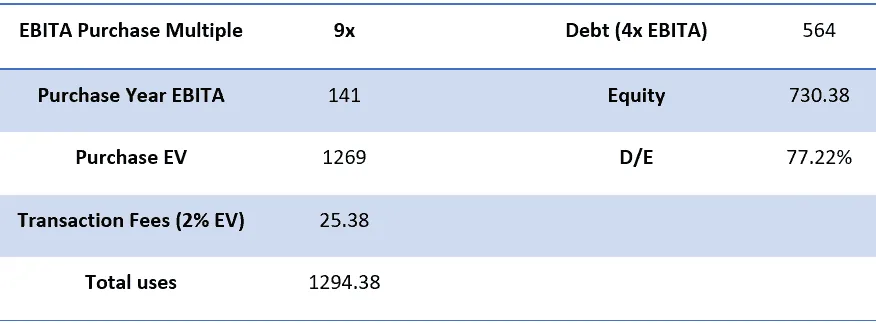

The first stage of deal capital structure would be a combination of equity and debt. The optimal structure should satisfy the main objective of maximizing the buyer’s benefit. Thus, a capital structure with the lowest weighted average cost of capital (WACC) would provide the highest NPV. Appendix 1 shows the Multiple analysis.

Appendix 1: Multiple Analysis

The EBITA multiple based on Morgan Stanley’s point of view is used in this analysis. The EBITA multiple to determine Enterprise Value is

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.