RJR Nabisco - Case Solution

This RJR Nabisco case study analysis looks deeper into how the stream of FCFs and tax shields were determined for the three different valuations methods, which are APV, WACC, and CAPV.

Case questions answered:

- For each of the three plans (Prebid, Management, and KKR): a) Calculate the free cash flow for each year b) Estimate the tax shield for each year c) Estimate the unlevered discount rate d) Value RJR Nabisco

- Estimate the stock price of RJR under each of these plans.

RJR Nabisco Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

RJR Nabisco Firm Value Calculations - Details and Assumptions

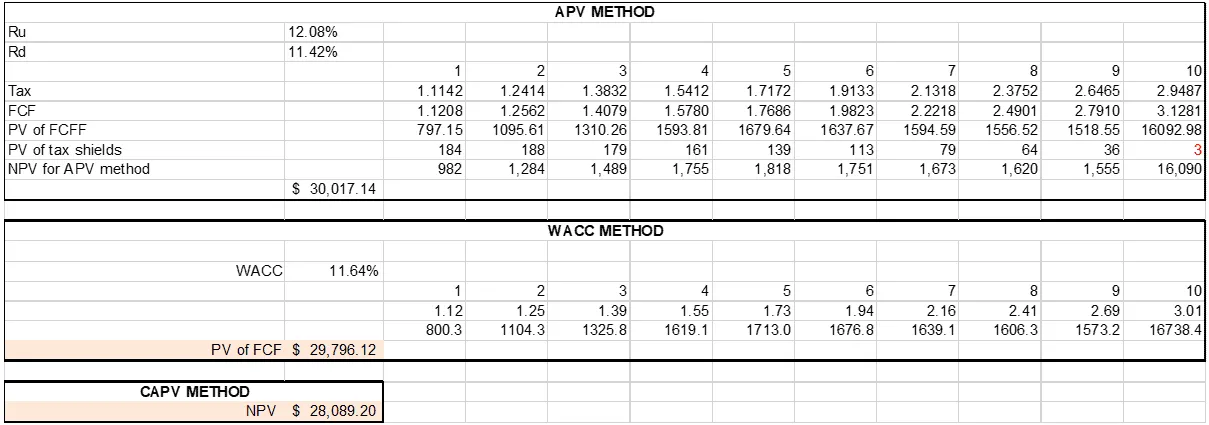

The value of the firm RJR Nabisco has been evaluated for three different scenarios using three different valuation methods, which are APV, WACC, and CAPV.This report delves deeper into how the stream of FCFs and tax shields were determined for these methods.

Estimation of Tax Rates for each of the three buyout proposals:

- Prebid – To calculate Profit Before Taxes (PBT) for RJR Nabisco, we deduct the interest expense from EBIT. From PBT, Net Income is subtracted to calculate the taxes & tax rates for each year.

- Management and KKR – PBT is calculated as operating income minus the net of interest expense and amortization amount.

- Prebid – The EBIT numbers have been plugged from exhibit 5

- Management and KKR – EBIT numbers are calculated as Operating Income minus the Amortization value. For KKR, the noncash interest expense has been ignored.

The cash flows from the 11th year (1999 onwards) have been assumed using the cash flow of 1998 as a base with a growth rate of 3% (approx. GDP growth for the US). Hence, the discounted cash flows for the 10th year include the…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.