Hong Kong Dragon Airlines Limited (B): Lease vs. Buy Decision - Case Solution

Hong Kong Dragon Airlines Limited created a task force sometime in 2006 to look into better alternatives for replacing spare engines. The company was faced with two options. The company may opt to buy the engine outright or to rent the engine via a direct lease or a sale-and-leaseback arrangement. The task force must first identify the correct discount rate to use in order to come up with a comparison of the advantages of the two options.

Case questions answered:

- Review your weighted average cost of capital calculations from the Hong Kong Dragon Airlines Limited (A) case study.

- What are the after-tax cash flows relevant to the purchase of the V2533?

- What are the after-tax cash flows relevant to the sale and leaseback of the V2533? The Lease of the V2533 involves payments into two reserve funds (flight hour and flight cycle) described in the case. The size and timing of the payments are detailed in Exhibit 3. These reserve funds are like savings accounts, with the balances to apply toward any maintenance needed. The 2012 balance of the flight hour reserve can be applied toward the anticipated heavy maintenance in 2012. The flight cycle reserve funds will likely be lost as they don’t anticipate needing flight cycle-based maintenance during the period of time Dragon Air will need the engine.

- What are the qualitative issues associated with the options given in the case?

- Perform sensitivity analysis to identify the key bets/assumptions in your decision.

Hong Kong Dragon Airlines Limited (B): Lease vs. Buy Decision Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

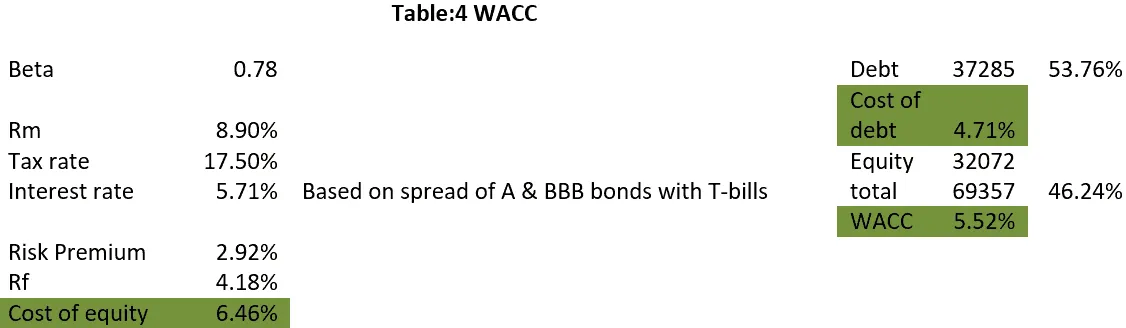

1. Review your weighted average cost of capital calculations from the Hong Kong Dragon Airlines Limited (A) case study.

In reviewing the weighted average cost of capital from the Hong Kong Dragon Airlines Limited (B) case study, I chose to use 5.52% as the WACC.

For the cost of equity, I used 6.46%, and for the after-tax cost of debt, I used 4.71%. For the weights, I used the averages of debt and equity for weights of 53.76% debt and 46.24% equity.

2. What are after-tax cash flows relevant to the purchase of the V2533?

The After-tax cash flows relevant to the purchase of the V2533 include the outflows for the capital expenditures in 2006 & 2007, along with any maintenance costs.

The Cash inflows include the yearly tax savings for ten years, which is the sum of any maintenance cost and depreciation times the companies’ tax rate.

In 2017, the company was able to sell the engine for a residual value of around $2.75 Million, creating an…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.