Fojtasek Companies and Heritage Partners--March 1995 - Case Solution

The Fojtasek Companies is a family business and one of the issues it has to address is the issue of generational succession. It is confronted with several financing choices like buyouts that have expressed their interest in taking over the firm by acquisition, a proposed leveraged recapitalization from an investment bank, and a hybrid transaction from a private equity group named Heritage Partners.

Case questions answered:

- What is the Fojtasek Companies' problem? How does each of the three possibilities – a buyout, a leveraged recapitalization, and a private IPO – address the family’s needs? What are the major concerns for them with each transaction?

- Is Fojtasek an attractive transaction for Heritage qualitatively? Quantitatively? Your qualitative analysis should discuss the qualitative desirability of the company. Your quantitative analysis should include a DCF analysis and an IRR analysis for Heritage’s investors.

- How reasonable is the payment for Fojtasek Companies being offered by Heritage? How onerous are the control rights Heritage is demanding? What should the Fojtasek family do? Should they accept the $56 million Heritage offer, accept the $65 million LBO offer, or reject both offers?

- Is the Fojtasek family’s problem a common one? Does the “Private IPO” solve it?

- As an institutional investor, would you invest in Heritage Partners? What is Heritage’s partnership strategy? What is distinctive about it? Do you think Heritage will earn abnormally positive returns? Would Swensen invest in Heritage?

- What were the problems that the family faced?

- Mention the pros and cons of the 3 options - Buyout, Leveraged Recapitalization, Private IPO.

- Should the family accept the offer from Heritage?

- Is the model applicable to family-owned businesses in developing markets and countries?

Fojtasek Companies and Heritage Partners–March 1995 Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

You will receive access to two case study solutions! The second is not yet visible in the preview.

1. What is the Fojtasek family’s problem? How does each of the three possibilities – a buyout, a leveraged recapitalization, and a private IPO – address the family’s needs? What are the major concerns for them with each transaction?

Having experienced substantial growth over the past years, the Fojtasek Companies seem to have successfully managed the period of management transition, which started in 1992. However, the family still had to deal with the transformation of ownership.

Three of the children had voiced interest in liquidating their stake in the company, and the Fojtaseks had to plan how they would deal with the burden of the inheritance tax when the ownership of Joe Fojtasek is transferred to the new generation.

In finding a solution to these significant upcoming capital needs, the different family members were pursuing different interests. The ones interested in liquidating their stake would benefit most from a high selling price. At the same time, the new CEO, Randall Fojtasek, was concerned with retaining control of the company and maintaining its future growth prospects. The Fojtasek family, therefore, faces the decision of which solution best fits everyone’s needs – buyout, leveraged recapitalization, or private IPO.

Fojtasek companies received buyout offers ranging from $ 58 to 62 million, promising a higher immediate payout to the firm’s shareholders than the other alternatives would. A buyout fund could potentially restructure the firm radically, making the future of the company’s long-time employees uncertain but also making the family’s involvement, particularly that of the CEO, unclear.

As buyout structures would include a high degree of leverage, strong restrictions on the firm’s financial flexibility would be imposed. These restrictions could potentially hurt the firm’s growth potential, as arising acquisition opportunities might have to be forgone if the necessary financial firepower is missing.

By pursuing a leveraged recapitalization, the company would face similar issues regarding flexibility constraints imposed by high degrees of leverage. It would, however, allow the Fojtasek family to retain ownership of and hence control over the company.

While the leveraged recapitalization seems to tackle some concerns of Randall Fojtasek, the family members wanting to liquidate their stake are most likely worse off compared to a buyout solution.

Reimbursement of their ownership share would be subject to higher taxes, as it would be treated as dividends rather than capital gain. The amount of equity that can be extracted from the company is also uncertain, as banks might be unwilling to lend substantial amounts of capital to the company for the sole purpose of paying shareholders.

Finally, just as a leveraged buyout, a leveraged recapitalization would increase the risk of default in the case of an economic downturn.

A private IPO with Heritage Partners is the third option available to the Fojtasek family. It would offer a significantly lower transaction value compared to an LBO, potentially making departing shareholders worse off. The tax treatment of cash proceeds to shareholders as capital gains would, however, be more beneficial compared to a leveraged recapitalization.

The private IPO structure would involve lower levels of leverage, allowing the firm to maintain some of its flexibility in pursuing growth opportunities. Initially, the family would retain a majority ownership stake in the firm (50.1% common equity), which, however, doesn’t translate into full control over the firm, as envisioned amendments of the by-laws would require a supermajority (~60%) for critical management decisions.

Furthermore, the fund would hold preferred shares, which, in case of poor performance, would convert into common shares, bringing the fund’s stake up to 65%, hence putting it in full control over the company.

2. Is the Fojtasek Companies an attractive transaction for Heritage qualitatively? Quantitatively? Your qualitative analysis should discuss the qualitative desirability of the company. Your quantitative analysis should include a DCF analysis and an IRR analysis for Heritage’s investors.

Heritage is targeting mature and successful family businesses with sales ideally ranging from $50-150m and stable profits in low cyclicality industries that are not high-tech or research-intensive. Fojtasek falls within those qualifications.

The building materials market is closely tied to the cyclical housing market, which is balanced through the countercyclical repair and remodeling market. The building materials business is relatively low-tech and less intensive in terms of research.

Fojtasek is among the top 10 most significant manufacturers and distributors of wood, aluminum, and vinyl building materials. In their core markets, they hold market shares of approx. 25%, indicating a dominant market position. This value, on the other hand, also means that there is ample growth potential as Fojtasek’s business is still quite localized.

Moreover, recently introduced aluminum windows and newly opened vinyl manufacturing sites provide significant market penetration and growth opportunities, especially concerning an expansion to the north of the US, as vinyl is the fastest-growing segment among the markets Fojtasek operates in.

What may also help in this regard is that Fojtasek has powerful brand recognition within its core market, the home builders. Fojtasek is also operating in a highly fragmented market that only sees the beginning of consolidation action. There is a wide range of M&A opportunities that can be accessed with fresh capital provided by investors and significantly enhance both market position and economies of scale as Heritage (or, more correctly, Equity Partners) has done in the past with other investments.

However, the Baloleum division should also be considered as it has seen revenues decline over the years and depicts a significant struggle. On the other hand, this could be a source of potential value creation as Heritage might want to restructure the division and use the current shape as a source of “underpricing” of Fojtasek, leaving considerable upside.

Furthermore, opportunities for cost savings exist by integrating manufacturing and executive functions across divisions. In addition to that, the current management team has a proven track record. It is led by the Fojtasek family, implying that the major portion of their private wealth is tied to the company, ensuring aligned incentives.

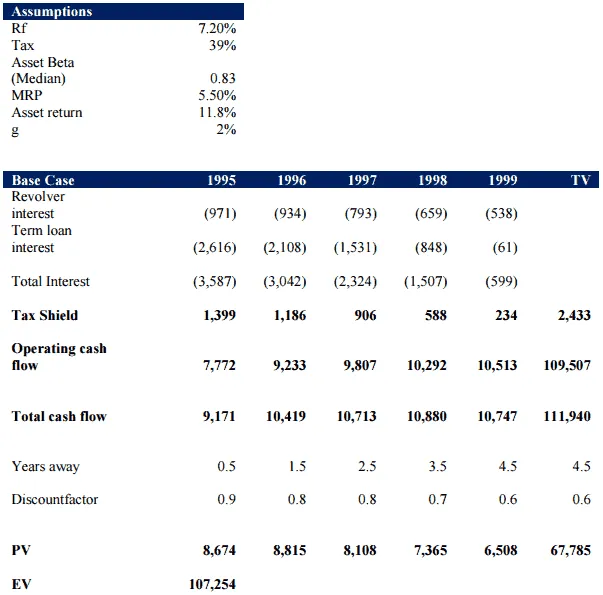

The transaction values Fojtasek at $56m. When comparing this to regular valuation metrics, it seems like this transaction depicts a very good deal for Heritage investors. A regular APV valuation based on the base and management case yields a value of $107m and $130m, respectively, significantly above the bids offered by Heritage and other buyout groups (see Exhibit 1).

Exhibit 1. APV Analysis

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.