First American Bank: Credit Default Swaps - Case Solution

First American Bank: Credit Default Swaps case study looks at FAB's management of credit exposure. Should the bank hold on to the credit risk of CapEx Unlimited, one of its clients?

Case questions answered:

- What is a credit default swap? How does it work?

- What would be the fair level for the semi-annual fixed fee on the default swap? a.) What is the probability of default for CapEx Unlimited (CEU)? b.) What are the expected cash flows for the default swap? c.) What discount rate should be used to discount the expected cash flows? (hint: probabilities of default in the Merton model are risk-neutral probabilities.)

- Should First American Bank hold on to the credit risk of CEU? How can this risk be transferred away from FAB’s balance sheet?

- What are the different approaches to managing one’s own credit risk?

First American Bank: Credit Default Swaps Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

1. What is a credit default swap? How does it work?

A (credit) default swap is essentially protection that can be bought by one party from another to ensure against certain credit events, often defaults. The protection buyer pays a periodic fee (similar to an insurance premium) to the protection seller.

Such payment continues until the expiration of the contract or the occurrence of a credit event. This periodic fee is in exchange for credit protection, in which the protection seller is obligated to be contingent on a specified credit event taking place.

Credit default swaps were standardized in the late 1990s by the International Swaps and Derivatives Association (ISDA). This standardization brings several benefits, including the increased speed with which deals can be executed and the minimization of “documentation risk” caused by varying definitions and contracts. These instruments allow the splitting up of the types of risk exposure to a credit obligation.

By selling protection, an investor is essentially isolating the default risk of the security and does not have to deal with other credit risks, such as interest rate risk. It furthermore allows risk to be spread among a wider class of investors looking for exposure here, which has the effect of extending the availability of credit for those seeking it.

2. What would be the fair level for the semi-annual fixed fee on the default swap?

a.) What is the probability of default for CapEx Unlimited (CEU)?

Charles Bank International (CBI) was recurring in a credit default swap with First American Bank (FAB) because they wanted to look for protection on the additional loan that they were willing to give CapEx Unlimited (CEU) for maintaining their banking relationship.

A pricing model was needed to value only the credit default swap on the risky portion of the debt (isolating the credit risk on the additional loan). The terms of the new loan included a coupon rate of approximately 9.8% and a maturity of two years.

According to Exhibit 10b, CEU’s probability of default in two years will be 13.70%, given that CEU’s publicly traded debt rating was B2 from Moody’s. In addition to this, According to Exhibit 10a on Historical Default Rates between 1970 and 2000, technology companies’ average yearly default probability was 1.24%.

We could come up with a CEU’s default probability out of historical data. However, we aim to value a credit derivative instrument. It means that we should use risk-neutral probabilities instead of historical data, which leads to using a structural approach for this credit risk modeling based on the Merton Model (using the Black-Scholes option pricing formula).

We know from the case that the total market value of equity is equal to $6.8 billion and that debt has a total market value of approximately $4.1 billion. Hence, the total market value of CEU is $ 10.9 billion.

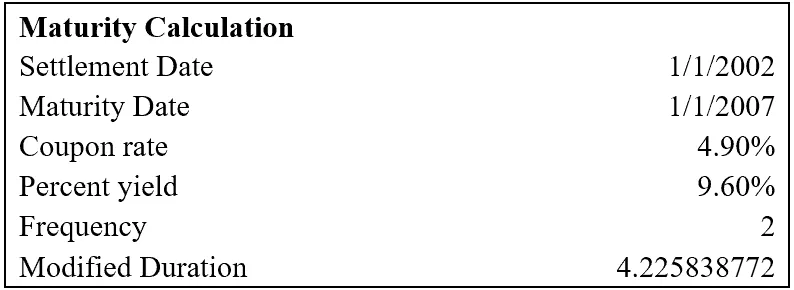

To use the Black-Scholes option pricing model, we need to define a maturity, which we calculated as the Modified Duration (MDURATION Function in Excel). The calculation goes as follows (please refer to the attached Excel file):

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.