Facebook, Inc.: The Initial Public Offering - Case Solution

In mid-May 2012, the pricing of Facebook Inc.'s initial public offering (IPO) was undertaken. A CXTechnology Fund analyst looked forward to speaking with the lead underwriter about his interest after a review of Facebook Inc's phenomenal growth as well as its potential for profit as a business and in the competitive environment of social networking. The analyst had to come up with the decision whether to subscribe to shares in the IPO or not, considering that the IPO appeared to be oversubscribed with heavy interest, and the valuation seemed to be much more.

Case questions answered:

- Why is Facebook going public? How much money would the company raise from the IPO? What is the planned use of proceeds from the offering?

- Exhibit 11 provides an estimate for Facebook’s share value using DCF. How sensitive is the valuation to assumptions on revenue growth, margin, and the WACC? Do you agree with these assumptions? If not, how would the valuation change based on your modification?

- Provide an estimate for Facebook’s share value using market multiples. Explain your choice of comparable firms and multiples.

- As a potential shareholder, do you have any concerns about Facebook or its stock offering?

- The Ultimate Question: Do you recommend CXT to invest in Facebook’s initial public offering given the current price talk ($34 - $38)?

- How does Facebook Inc. make money? What are the value drivers of its business? What is its comparative advantage relative to other social networking companies?

- Why is Facebook going public? What is the planned use of proceeds from the offering?

- What was going on in the U.S. IPO markets prior to Facebook’s offering? What has been the performance of recent IPOs?

- What is the intrinsic value of a Facebook share? How does the valuation compare to the price talk from the underwriter?

- As a potential shareholder, what are your concerns about Facebook or its stock offering?

- What is your recommendation for the CXT Technology Fund?

Facebook, Inc.: The Initial Public Offering Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

You will receive access to two case study solutions! The second is not yet visible in the preview.

Executive Summary - Facebook, Inc.

Facebook Inc. is a social media application that Mark Zuckerberg founded in February 2004. The app was designed to use modern science and technology that allowed users to connect with people around the world.

Facebook’s users had increased drastically from 500 million in 2010 to 900 million in 2012. Based on the rising popularity and publicity of Facebook, it was merely a question of time before the company went public.

As Facebook planned to go public, the initial stock price range was between the $20s to mid-$30s per share; however, the price talk had raised its IPO price to $34 to $38 per share.

The chief analyst of CXTechnology Fund, McNeil, judged the riskiness of overpaying Facebook’s IPO price. Yet, he did not want to miss this substantial opportunity, which could make CXTechnology profitable as well.

For this reason, McNeil would like to recommend that CXTechnology should invest in Facebook’s IPO and a proper price range of the stock.

Problem Overview

There are two main reasons why Facebook Inc. had to go public.

First of all, “the principal purposes of the IPO were to create a public market for the existing shareholders and to enable future access to the public equity markets” (case p.2). To be more specific, by going public, Facebook can raise funds from a broader pool of investors.

Using these funds, Facebook can develop additional capital or products that can make the company more competitive. By going public, Facebook can attract more investors to join the company to increase its funds and expand its market share.

In addition, mobile users have been an important contributor to Facebook’s growth, reaching 483 million daily active users worldwide in 2011.

Before the IPO, Facebook was unable to show ads to mobile users. Facebook needed to find a solution before it threatened to cannibalize the company’s advertising revenue.

Another reason IPO is attractive to Facebook is that the fees for underwriting listings were just 1.1 percent because of the growing prestige of the offering, compared with the typical 3 to 7 percent of the amount raised for equity IPO.

The underwriters also gave Facebook Inc. an overallotment option (“greenshoe”) to sell an additional 15% of the offering, up to 484 million shares (case p.7).

Another essential reason is that there were too many shareholders, which passed 500 million by 2010.

An antiquated Securities and Exchange Commission rule from 1964 says that “any private company with more than 500 ‘shareholders of record’ must adhere to the same financial disclosure requirements that public companies do, which means submitting detailed quarterly and annual financial reports, and dealing with all the scrutiny that powerful companies face when they open their books” (Paul Sloan).

Facebook would raise $6.1-6.8 billion from the IPO. According to the case, Facebook was willing to sell $421,233,612 shares and sold its shares at $34-38. The number of shares was made up of issuing 180,000,000 shares and 241,233,615 shares sold by existing stockholders.

Therefore, the total money raised from the IPO equaled the total number of shares multiplied by the price per share, whose result was also the same as $6.1-6.8 billion in the case.

According to the case, the planned use proceeds will be used for working capital and other general corporate purposes.

We estimated the other general corporate purposes would be operating expenses (which included the costs of broadening the number of users, research and development costs), acquisition costs, and investment costs (such as bonds and money market funds). Other potential costs may be the cost in which Facebook Inc. figures out a solution that allows ads to be displayed on mobile devices.

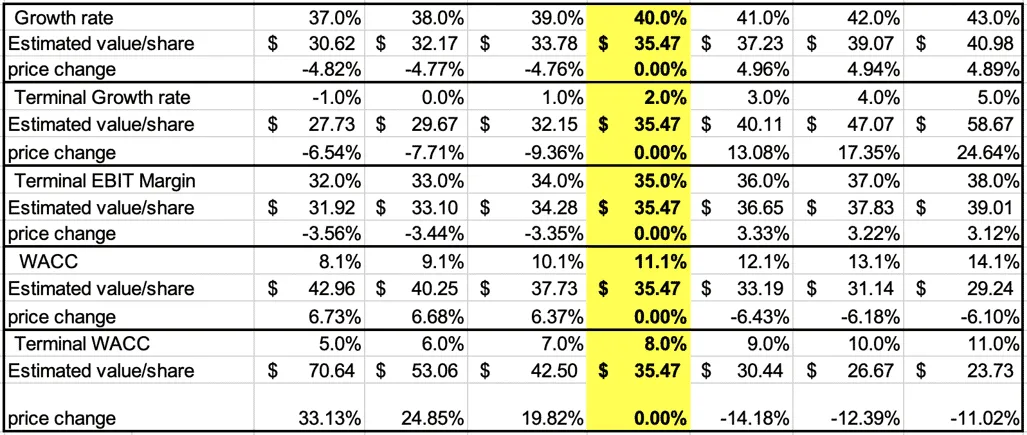

Original Sensitivity Analysis

Based on the DCF Valuation from the case, we did a sensitivity analysis on the assumptions of growth rate, terminal growth rate, terminal EBIT Margin, WACC, and terminal WACC.

We chose a 1% increase and decrease based on the case assumptions, then calculated the price change with each one percent change in those assumption values.

Table 1 shows the price change when each variable increases or decreases by 1%. Facebook’s estimated value/share was $35.47 based on Professor Aswath Damodaran’s assumptions.

Table 1: Sensitivity Analysis Based on Case Assumptions

To compare which variable has the highest sensitivity to Facebook Inc.’s stock price, we made a graph for the stock price change based on a…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.