Dell's Working Capital - Case Solution

Dell Computer Corp. produces, sells, and services personal computers. Dell utilizes the build-to-order scheme by taking orders directly from customers through phone calls. The company then delivers the computers directly to the customers. This scheme is advantageous for Dell since it requires a smaller investment in working capital as compared to its competitors. Thus, Dell has rapidly developed and has relied on internal sources to finance its growth. This case study about Dell Corporation focuses on the advantage of proper management of working capital in a fast-developing company.

Case questions answered:

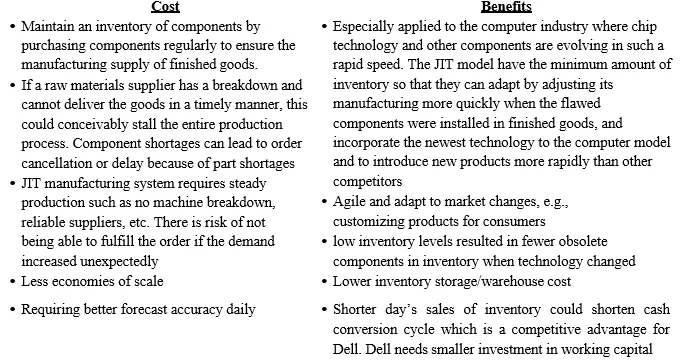

- What are the costs and benefits of Dell’s just-in-time manufacturing system?

- Suppose that you are now in the planning stage for fiscal 1996 and that you estimate that in fiscal 1996, sales will grow 52%. (This is the actual growth rate.) If Dell’s operation in fiscal 1996 were to repeat the fiscal 1995 operation, what would be the external financing needs? Compare your forecast to the actual performance in the fiscal year 1996.

- Assume that Dell will grow 50% in fiscal 1997. How would you recommend that Dell finance this growth? Will it be possible for Dell to finance the growth without accessing external funds? How much working capital would Dell need to be reduced and/or profit margin increased? What steps do you recommend the company take? Base your forecasts on the 1996 performance.

- Analyze Dell's working capital policy.

- Analyze the financing of the 1996 expansion.

- Analyze if Dell can finance its 1997 expansion, expecting a similar growth to that in 1996.

Dell's Working Capital Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

You will receive access to two case study solutions! The second is not yet visible in the preview.

Dell’s Working Capital Case Memo

The purpose of Dell’s Working Capital Case Memo is to address how Dell Computer Corporation could best finance its anticipated double-digit growth in a rapidly changing industry at the time of 1996. Dell gained impressive growth from 1991 to 1995 with a CAGR of ~56%, far beyond its competitors.

The success was attributable to Dell’s direct-to-consumer (D2C) strategy and build-to-order model that yielded low inventory balances. One of the key takeaways from the cost and benefit analysis (Exhibit 1) on Dell’s manufacturing model is that Dell should have advantages in cash management over its competitors.

Exhibit 1 – Cost and Benefit Analysis of Dell’s Just-In-Time Manufacturing Model

To better understand the financing options for Dell in 1996, we reviewed its operation retrospectively. We applied the 52% growth rate to the sales, actual cash, working capital, and PPE from the 1995 balance sheet of Dell Corporation. The other items, such as other current assets and long-term debt, were assumed to be the same as those in 1995.

As Dell shifted their focus to profitability in 1993 and had competitive advantages due to the leading Pentium technology, we assumed the net profit in 1996 would grow proportionally at a rate of 52%.

Under these key assumptions, Dell would need $80M as an additional fund to sustain the growth and maintain the same operation (Exhibit 2). Comparing our pro forma statements with the actual performance in 1996, we noticed a few major differences:

- Dell did not finance the growth by borrowing additional bank loans; instead, it issued common equity to raise funds. The composition of capital structure shifted towards the more common stock.

- Dell’s $272M actual net profit is $45M more than the pro forma. The higher margin is aligned with the fact that sales shifted from 71% for older models to 75% for the more profitable Pentium models.

- Dell increased their short-term investment significantly from $484M to $591M, reflecting its increasing focus on liquidity.

- Dell shortened the receivable outstanding from 57 to 50 days, reducing payable outstanding from 54 to 40 days. The number of days sales of inventory was also trending down from 39 to 37 days (Exhibit 3). Although each item of working capital seemed to be better managed, CCC increased by 5 days, which led to the need for an $80M fund.

Following the same assumptions in the 1996 pro forma analysis, we applied a 50% sales growth rate to the actual FY 1996 financial statements (Exhibit 4) to arrive at pro forma statements for 1997.

Without adjusting profit margin and working capital, Dell will need…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.