Cost analysis of patio furniture: Leisure Products (LP) - Case Solution

Leisure Products (LP) is a company that manufactures various types of furniture (lawn and Patio) which are sold in warehouse stores, retail hardware and departmental store chains. The company is faced with some critical decisions to make regarding one-time special order at a lower cost from a customer- Southeast departmental stores.

Case questions answered:

- Calculate the incremental variable, or marginal, cost per chair to Leisure Products (LP) of accepting the order from Southeast.

- Based on the above, should LP accept the Southeast order?

- What additional considerations might lead LP to reject the order?

Cost analysis of patio furniture - Leisure products (LP) Case Answers

Summary - Leisure products (LP)

Leisure Products (LP) is a company that manufactures various types of furniture (lawn and patio), which are sold in warehouse stores, retail hardware, and departmental store chains.

The company is faced with some critical decisions to make regarding one-time special orders at a lower cost from a customer- Southeast departmental stores. Southeast company wants to purchase 30,000 units of chairs from Leisure Products for August delivery.

There are several factors that the company must consider and analyze before accepting or rejecting the order to arrive at the best short-term decision or alternative choices.

Some of the factors to consider in the analysis are the relevant and irrelevant costs, incremental revenues, and incremental costs, and they must be properly evaluated.

Problem and/or Issue Faced by Leisure Products

The situation at hand facing Leisure Products company is basically whether to accept or reject the special order. The Leisure management and accountant feel that the firm should not accept the order.

On the other hand, the economist thinks that the company should accept the order if the incremental revenue exceeds the incremental costs.

For the Leisure company to arrive at the best decision, the management must look for possible actions or solutions, such as performing incremental analysis.

Solution- Incremental analysis for Leisure Products

Using an incremental analysis approach can help Leisure Products management to make this important decision. The Leisure company received a special order from Southeast Company for the purchase of 30,000 units of chairs.

Next year’s planned production is 500,000 units of chairs to be sold at $7.15, but the customer has requested a lower price of $5.50.

It is mentioned that Leisure Products can produce the chairs during a slow period between June and August. It means that the company has adequate capacity to manufacture an additional 30,000 units and enough workforce.

By looking at this information without going into details, it may seem that the Southeast order should be rejected. The order’s selling price is $ 5.50, but the chairs cost $7.15 to manufacture and sell, resulting in a loss of $1.65 for each unit/chair sold.

However, carrying out incremental analysis and reviewing all the relevant costs and revenues may give a totally different result.

Determining the incremental revenue for Leisure Products

Southeast is planning to order 30,000 chairs if the price does not exceed $ 5.50 for each unit/chair.

30,000 * $5.50= $165,000

The sales of 30,000 units at $5.50 will increase the revenue by $ 165,000 and is relevant in making this decision.

This order will not affect the current business of Leisure Products, so the planned production and sales of 500,000 units to be sold at $7.15 is not incremental as it will produce the same revenue regardless of whether the Southeast order is accepted or not. Therefore, $7.15 is a sunk cost because it is not avoidable.

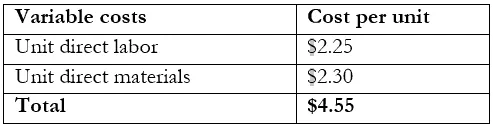

Determining the incremental variable costs

When 30,000 units are produced, the company will incur materials and labor costs and consider the relevant costs.

It is assumed that all the plant overhead and administrative and selling expenses are fixed costs. It is also important to know what proportion of these costs, if they exist, represent variable costs.

For example, a section of the plant overhead, such as supplies and power, are variable costs, and they vary with the output level.

Likewise, part of the selling and administrative costs of Leisure Products, like the billing costs, may constitute variable costs.

Total incremental variable costs

The total incremental variable costs are calculated by multiplying the unit cost by the 30,000 units/chairs in Southeast order.

Because variable costs are increased, profits will be decreased by these two incremental amounts. These incremental variable costs are shown as negative amounts in incremental analysis.

Determining incremental fixed costs

Fixed plant overhead and Administrative and selling expenses are not relevant because they will result in the same total amount no matter if the order is accepted or not.

Summary of costs (Incremental revenue and incremental costs)

Incremental revenue $165,000

Incremental costs

Direct labor ($67,500)

Direct materials ($69,000) $136,500

Incremental increase in profit if the order is accepted $28,500

Profit is expected to increase by $28,500 if the order is accepted.

Based on this incremental economic analysis, the Leisure Product company should accept the Southeast order.

Benefits of accepting Southeast order

- This is because the incremental revenue exceeds the incremental costs, and it represents an increase in profit for choosing to accept the order; therefore, incremental profit will increase by $28,500.

- If the chairs will be produced during a period of reduced output, then excess capacity is available to accept the Southeast order. The company can take advantage of this instead of leaving capacity idle. So, the chief economist is right that Leisure products should accept the offer.

Rejecting the order (disadvantages of accepting the order)

On the other hand, if Leisure Products decides to take the chief accountant’s advice to reject the order, then some of the considerations that might lead to rejection would be;

- In case extra raw materials are needed to produce the 30,000 units of chairs, then the Leisure company will incur additional variable operating costs.

- Some of the next year’s sales of 500,000 units of chairs in other markets might be affected by the special order.

- A regular customer might find out that an order was accepted at a lower price and might demand a lower price regularly.

- The Southeast special order might start a price war with the competitors in the market.

Benefits of carrying out incremental analysis

- It helps make quicker, simpler, and more effective business decisions because once relevant costs are identified and separated into variable and fixed costs, it becomes easy to solve the problem and make better decisions.

- It gives accurate results that are important and adequate to choose the best alternative with the available information.

- It also shows the effects that are likely to be making a business decision.

Conclusion

Incremental analysis is the best tool, especially for managers facing tough business decision-making on a regular basis. It can summarize the major benefits, disadvantages, and consequences of the options available before making the final decision affecting the future income.