Breeden Security, Inc. (B) - Case Solution

Breeden Security, Inc. (B) case study focuses on Marlene Baer, the controller of Breeden Security USA, and her method of grouping overhead costs by activity and distributing them to the firm's two products which are not correct. This case study also discusses the activity-based costing system to allocate costs which helps in assessing both product and customer profitability.

Case questions answered:

- Using the case study as a starting point, prepare an analysis of the ABC system using, but not limited to, the following topics: • The usefulness of ABC for service firms • ABC cost models and their advantages over traditional cost models • The barriers to ABC implementation • The use of ABC systems to improve operations and to make better decisions about products and customers.

- The paper should include: • Introduction of Topic and Facts as presented in the case (paraphrased). The discussion of the case is grounded in the facts as presented. Therefore, you must discuss the facts as a starting point. • A summary of the area(s) of accounting (this area must conform to Generally Accepted Accounting Principles theory with examples to justify understanding). An accounting area is your understanding of a description of the topic area and what FASB states as the main points of the topic of accounting. • A Detailed Case Discussion. You must provide examples and sound rationale for your arguments. (In this section, you will discuss the case and include any topics required to be addressed in your assignment. Specifically, you should note the specific topics your instructor assigns as part of the case and document your responses in this section with a topic heading. • Conclusion (This is the general conclusion to the case and should not be integrated into your personal conclusion under the discussion section.)

Breeden Security, Inc. (B) Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

Introduction - Breeden Security, Inc.

Breeden Security is one of the leading German businesses that manufactures signal devices and radio equipment. The company also has operations globally, especially in the U.S. The company has a subsidiary that manufactures two products, RC1 and RC2.

These products recently achieved great success in the European market. After one year of operations, the company decided to revise its profit and cost performance. Breeden Security, Inc. hired a supervisor named Marlene Baer from its parent company in Germany to perform a deep cost and profit analysis.

Both of the products were more or less similar, but RC2 was more expensive than RC1 because of additional features. In the year 2008, the company forecasted that the demand for RC1 would be higher than the other products, but the actual results were shocking.

The demand for the RC2 was much higher than the anticipated demand. The staff was happy with the performance because the decrease in sales units of RC1 was settled with the increased unit sales of RC2.

The hired supervisor decided to study the factors that led to that significant change in anticipation. Moreover, Baer was looking forward to making some alterations in the facts and figures used previously to anticipate demand and costs.

Baer found out that the method used for the absorption of manufacturing overheads was based on direct labor, which was not an appropriate way to calculate the accurate cost.

This is because the manufacturing overhead for both of the products was using different amounts of resources and therefore, she could not use the same overhead rate to manufacture both products. She was confused to choose more accurate factors to allocate the manufacturing overheads accordingly.

After a bit of more research, she again favored the method of absorbing overheads based on direct labor. Later on, she also considered another costing method, “ABC,” for the calculation of the most accurate costs, but it was very difficult to identify cost-driven activities and factors.

Summary of Types of Accounting

The analysis is based on the costing approaches used in the case study. The two main costing methods, “absorption costing” and “Activity-based costing,” provide a detailed analysis of the company’s strengths and weaknesses in terms of estimated cost.

The analysis was done by Breeden Security, Inc.’s hired supervisor, which still has many points that need to be focused on again, but the positive side of her analysis includes the identification of cost-driven factors for ABC.

After she decided to consider ABC, the next step was to identify the factors that drive cost. In the following year, the manufacturing overhead was allocated according to her identification factors --- assembling, fabrication, packaging, and shipping --- on the percentage basis of direct labor. She preferred direct labor for manufacturing overhead allocation on all other factors, i.e., area and machine hours.

The reason she preferred labor over other factors was the attachment of labor with all other extra labor activities. That is why she suggested the method optimal for packaging and shipping. However, the use of direct labor resulted in an extra expense, which deducted a specific amount of cash flow from profit. Now, she has discovered that she can avoid these extra expenses by implementing the ABC method to get a clearer view of costs for Breeden Security, Inc.

Introduction to Activity-Based Costing (ABC)

ABC is an accounting model that identifies the activity centers in an organization and assigns costs to cost drivers, which is based on the number of each activity that occurred. The cost drives are based on those activities that have the highest number of occurrences at several levels (Derya Eren Akyol, 2007).

a) Unit level drivers - Increase in the number of inputs when each extra unit is produced.

b) Batch level drivers - Change in inputs when each additional batch is produced.

c) Product level drivers - The number of inputs required when an additional product is being produced in the firm.

d) Facility-level drivers - These are related to the facility manufacturing process.

In order to implement ABC, the following steps are important:1st) Identifying the activities such as machine, labor, serving, etc.

2nd) Determining the costs of each activity.

3rd) Determining the cost drivers, e.g., machining hours, labor hours, etc.

4th) Collecting the data of each activity.

5th) Computing the cost of product/service.

The usefulness of Activity-Based Costing for Service Firms

Service firms are facing many problems in finding an effective cost accounting system because the service does not have inventory to sell, and both direct material and direct labor are not major cost categories in the case of service firms.

Therefore, ABC helps firms like Breeden Security, Inc. to reduce and control costs to set the right price for making the company profitable. Some of these companies are in various industries like Financial Services, Health care, and Insurance. (Ruhl, 1998).

As service firms need a forward-looking costing system, ABC is a vital tool for such analysis. Service firms are more people-incentive and concentrate on activities used in order to focus on customer service.

Customer service is vital for the company’s success since a company’s major concern is to lower and control the “cost to serve.” (Chea, 2011).

ABC Cost Models and Their Advantages over Traditional Cost Models

Nowadays, Activity-based costing (ABC) has become an important tool of manufacturing/service sector firms, which measures the cost and performance of activities and resources (Derya Eren Akyol, 2007). Moreover, ABC answers questions like how is a product produced or how is a service served? How much time is needed? How much money the activity will require?

Moreover, ABC provides a more accurate method for costing products/services, which helps to price the product/service more accurately. It increases our understanding of cost drivers and overhead costs, which helps managers avoid using costly and non-value activities (CGMA, 2013).

On the other hand, the traditional method is more simplistic and less accurate than the ABC system. They typically assign a cost to products based on average rates, which do not give us proper detail. (OHIO University, n.d.)

ABC System to improve operation and to make better decisions about product and service

Using the ABC system can improve operational efficiency and helps companies make a better decision because of its nature to attribute costs by finding cost drivers associated with the activities.

- ABC system brings accuracy and reliability in determining product costs by focusing on cause-and-effect relationships of cost drivers and activities (Salem1, 2014).

- ABC helps in finding the more realistic cost per product.

- It identifies the real nature of cost behavior and helps managers in avoiding activities that do not add value to the product. Moreover, it uses more than one cost driver, which helps to trace the costs associated with the products.

- It further helps to rightly price the product, as it traces the cost of the product with more accuracy.

Case Analysis

a) ABC System to Find Answer Some important Questions

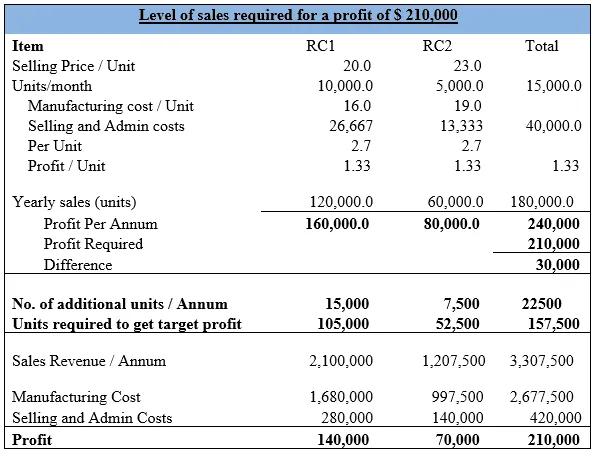

Level of sales will be required to achieve a target profit of $ 210,000

After calculation, it has been estimated that the difference is $ 30,000, which would have to be reduced from the profit margin. As per the current ratio of 2:1 of RC1 and RC2, the profit per unit is calculated at $ 1.33 / Unit.

The sales volume for the period is calculated below:

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.