Bancaja: Developing Customer Intelligence (A) - Case Solution

Bancaja is one of the top three financial institutions in Spain. This was due to the increased expansion in the 1990s. This caused it to expand too much and made it harder to control. The company values social responsibility, and repetitively shows that to its community. They are known for innovation and just introduced the concept of CRM and will conduct a pilot using credit cards.

Case questions answered:

- Is the credit card project appropriate for launching customer intelligence at Bancaja? Why or why not? What alternatives, if any, would you suggest?

- How would you design the project? (Consider questions like: How many attributes would you choose? Which ones? Why?)

- Which credit card would you commercialize? Why?

- How should Bancaja approach developing customer intelligence in the future?

Bancaja: Developing Customer Intelligence (A) Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

You will receive access to two case study solutions! The second is not yet visible in the preview.

Introduction - Bancaja: Developing Customer Intelligence (A) Case Study

Caja de Ahorros de Valencia was founded back in 1878 and is the parent company of Bancaja. Today, Bancaja is one of the most significant savings banks in Spain.

Throughout its long and rich history, Bancaja has prided itself on local service, patronage, and social responsibility. In the form of scholarships, conservation, and the arts, Bancaja has shown to the community that they are willing to give back to society.

Located in the third-largest city of Spain, Bancaja has 63% of its business coming from this financial hub. Over the years, Bancaja has spread its risk through multiple expansions, and interns created a very diverse portfolio consisting of real estate, insurance, investment services, and many more.

In 1989, they expanded by overtaking five banks in other areas in Valencia and continued to do so in the coming years. Today, Bancaja owns 656 branches throughout Spain. However, this has resulted in a ‘disjoined structure’ and created increased confusion within the organization and with its customers.

The company’s mission and vision are to address the unity of the Financial Group, cost efficiency, and the segmentation of industrial actions.

To tackle these problems, CEO García Checa has introduced the concept of Customer Relationship Management (CRM). CRM is targeted toward building a client base and increasing customer loyalty. This system created a lot of backlash from the local managers. Therefore, the company decided to conduct a trial run on credit cards.

Due to the low popularity of credit cards in Spain, the company has to find different ways of identifying and landing potential customers.

Throughout the case, with the help of marketing tools such as the 3 C’s, SWOT, Hofstede’s dimensions, and BCG matrix, I will outline possible expansion techniques within the credit card section and help design the optimal credit card with the help of CRM.

Due to this, Bancaja: Developing Customer Intelligence (A) is a decision case and will be treated accordingly.

3 C's

Company

Bancaja is one of the top three financial institutions in Spain. This was due to the increased expansion in the 1990s. This caused it to expand too much and made it harder to control.

The company values social responsibility and repetitively shows that to its community. They are known for innovation and just introduced the concept of CRM and will conduct a pilot using credit cards.

Competition

In credit cards, Bancaja is behind its competitors, with half the success rate and market share at 5% compared to 10%.

Additionally, their cards are also used half as often as their competitors. Increased competition has become a problem for Bancaja as it is cutting through its margins and market share.

Customers

The customers are mostly locals who are debt-averse, which causes them to take less advantage of the facilities, such as overdrafts, which leads to lower interest earnings for Bancaja.

Additionally, there have been complaints of confusing products like the revolving credit cards. Moreover, the culture adopts less electronic banking even though it seems to have become more popular.

SWOT

Strengths

The biggest strength of Bancaja is that they are the largest financial institution in Valencia and the third-largest in Spain. This gives them a clear advantage due to increased volumes and, eventually, economies of scale.

The parent company was founded in 1878, which could be associated with a more established brand image and a better understanding of the market.

As of 1996, the company owns 656 branches across Spain, which is due to the intensive expansion of acquiring five banks in 1989 and 4 more in the coming years. This has helped the company to diversify its product portfolio and, therefore, spread its risk through increased operations such as real estate, insurance, and investment services.

The main focus of this article is CRM, which the company adopted at an early stage, which will give them a competitive edge towards competition.

Additionally, Bancaja was one of the first to introduce the concept of revolving credit cards in the Spanish market. This gave them a competitive edge and created a reputation as an innovator.

Moreover, the company has a clear strategic vision and solutions in place to help achieve those visions. This will help reduce the confusion as both senior managers and employees will have an idea of what the company is heading towards.

Lastly, Bancaja provides scholarships and helps with the conservation of the arts. This is their way of giving back to the community, which will further help them improve their brand image.

Weaknesses

When CEO García Checa decided to adopt the CRM technique, he faced a lot of backlash from his employees. This scenario made it harder for him to sell the concept as “not all employees shared the CEO’s enthusiasm.”

This could also be the effect of the fact that the current CEO is not from a strong banking background. Therefore, the managers might not trust him, and they will blame him for the weaknesses of the company.

For example, a local manager said that their branch faced a customer overload and stated that “it was the CEO’s mistake and not the marketing officers.”

Additionally, due to the recent expansions, the company structure was ununified, which increased the time lags and added communication barriers. The new divisions didn’t seem to fit into the company’s organizational structure, which could have reduced employee morale and, therefore, productivity.

Even though Bancaja is the third-largest financial institution, it still has cost structures similar to smaller banks operating on lower volumes. This shows that Bancaja hasn’t optimally utilized the possible economies of scale that other banks closer to Banacja’s size are benefiting from.

Due to the high number of mergers and takeovers, the company’s initial united front had been compromised. Even though introducing the revolving credit card created a reputation of innovation within Bancaja, it was highly unsuccessful due to the complexity and both customers and employees not completely understanding how it works.

Opportunities

Bancaja is noted for having high costs not consistent with banks their size. To increase revenue and reduce costs, Bancaja needs to increase the volumes in which they provide their service.

To do this, Bancaja needs to improve its client base and increase customer loyalty. This action will solve one of Bancaja’s most prominent problems of being cost-effective.

Additionally, there is high growth in the credit card market as the world is progressing towards a more tech-savvy generation (Gen Z), which started in 1995. This growth has increased the demand for electronic banking, which is essentially the industry in which Bancaja operates.

Spanish people, on average, hold more credit cards than any country in the EU, and this could be an excellent opportunity for Bancaja to improve its sales. Complement this with Spain having the densest point of sale terminals, making it easier for customers to receive services.

Additionally, Spain has the second most number of ATMs, which further makes it easier for customers to access their money.

Moreover, the most significant opportunity for Bancaja is the increased number of revenue streams that will come about from introducing credit cards. They will have increased revenue streams in the form of signing fees, annual fees, and interest expenses. This might help them reach the critical mass and volume they need to achieve higher economies of scale.

Threats

The Spanish community is known to be debt-averse, which causes them to use cash more often than electronic banking methods. This could cost Bancaja a considerable portion of their business (Socioeconomic factors).

Additionally, due to the risk-averse attitude in 1996, 78.4% of customers paid their outstanding debt at the end of the month, which reduced the interest revenue that Bancaja would have earned otherwise.

Moreover, the market is facing increased competition, which is forcing them to reduce their costs and provide their services at lower margins.

Bancaja already has exceptionally high prices, and lowering margins will not sit well for them. This can also be seen in Appendix 4, where earnings before taxes for Bancaja are significantly lower.

One of the biggest threats for Bancaja is that even though they have the highest average number of credit cards per person in the EU, they fall short in the usage of those credit cards.

In Spain, the average use of a credit card per customer is 3.5%, whereas the EU average is 6.5, and in debit cards, Spain is at 4%, whereas the EU average is 14.2. This could be a massive threat to the sales revenue of Bancaja.

These factors are undercutting Bancaja’s sales revenue and margins, which could make it harder for them to sustain in the market.

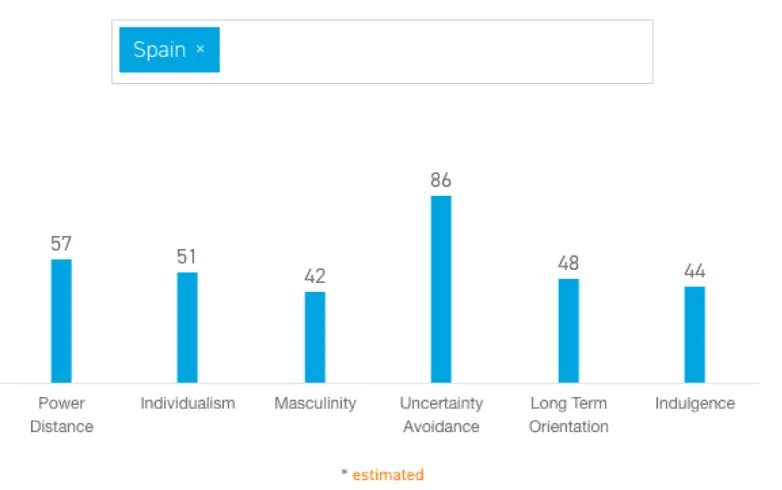

Hofstede’s dimensions

Hofstede’s dimensions show a great understanding of how a particular society functions and what values and norms it adopts. Spain has a really high uncertainty avoidance at 86, which is the main reason for the debt-averse culture they have.

High uncertainty avoidance shows that members of society are worried if they don’t know what the future holds. This is why upwards of 75% of Bancaja’s customers pay their remaining balance at the end of the month.

Next is individualism. As can be seen, Spain has a low individualism score of 51, which means that the degree of independence is low, and there is more of a close-knit family culture. Knowledge of such things can prove advantageous for Bancaja, as they could…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.