AQR's Momentum Funds (A) - Case Solution

In the AQR case study, a hedge fund plans to offer an investment strategy that uses the price phenomenon known as momentum to retail investors. However, the open-end and regulatory features of a mutual fund pose challenges to this strategy.

Case questions answered:

- Analyze Ken French’s 10 Momentum Portfolios

- Does momentum work?

- Should AQR launch its momentum funds?

- What is the source of momentum’s double-digit average returns? What evidence might help you decide what explains those returns?

- Do you believe the Fama-French momentum (UMD/MOM) factor will have returns over the next decade that are significantly greater than zero, significantly less than zero, or approximately zero? Use the historical data to do your analysis and come to class prepared to defend your conclusion.

- Compare the UMD factor to other specifications for momentum. Specifically, use the Spreadsheet Supplement for the case (which contains the momentum decile returns from Exhibit 3 along with the time series of the UMD return) to create: a. Decile Spread portfolio returns = (10-1) b. Quintile Spread portfolio returns = ((10+9)-(1+2)) c. UMD spread portfolio returns (given in Spreadsheet Supplement) d. Median Spread portfolio returns = (10+...+6)-(1+...+5)) Generate the average returns for each four of these momentum for every decade (the 1920s, 1930s, etc.). Does this affect your answer to (3) above?

- What are the appropriate benchmarks for AQR's Momentum Funds? Will the net performance of the funds exceed those benchmarks? Why or why not?

- The advantageous correlation structure in Exhibit 5 was seen as a key selling point of momentum. Is this the right way to think about AQR’s Momentum mutual funds? If not, use the data in the Spreadsheet Supplement to construct a more informative set of correlations. Does anything in AQR’s story change?

AQR's Momentum Funds (A) Case Answers

We have uploaded two case study solutions! The second is not yet visible in the preview.

Summary - AQR's Momentum Funds:

AQR was established in 1998 and is headquartered in Greenwich, CT. In early 2009, AQR was considering the launch of three new retail mutual funds that would offer retail investors exposure to AQR’s Momentum Funds.

Momentum is an effect in the market that investments that have performed well will continue to perform well, and those that have performed poorly will continue to perform poorly.

Therefore, a momentum strategy is when a fund takes a long position in an asset that has shown an upward trending price and short-sell security that has been in a downtrend. The positions in the fund will be adjusted according to recent performances.

This new momentum strategy is open to all investors and will be sold with the help of financial advisors. Our task is to figure out whether this strategy works well and a series of problems, such as benchmarks and challenges, faced by AQR.

Momentum Investment Strategy:

Momentum investing is an investment strategy that aims to capitalize on the continuance of existing trends in the market. To participate in momentum investing, a trader takes a long position in an asset that has shown an upward trending price, or the trader short-sells a security that has been in a downtrend.

The basic idea is that once a trend is established, it is more likely to continue in that direction than to move against the trend.

On the surface, investing strategies based on momentum are quite appealing: Buy stocks that have recently performed the best and avoid those that have been big losers. In other words, the strategy calls for us to act just as our emotions would have us behave.

Quantitative Analysis:

1. Analyze Ken French’s 10 Momentum Portfolios

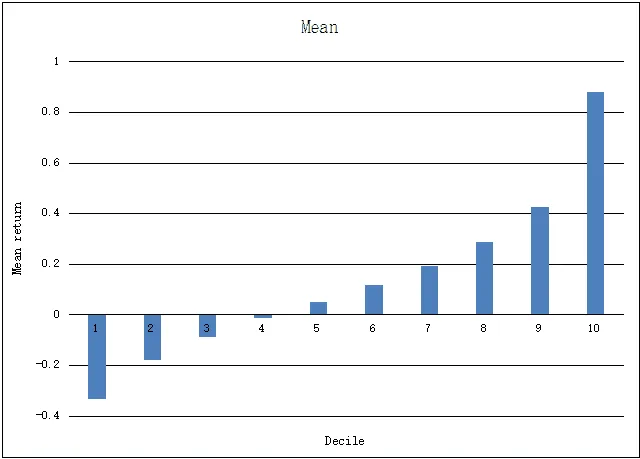

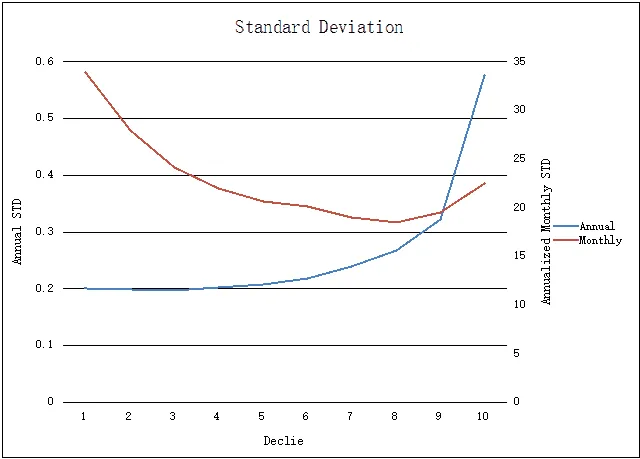

At first glance of Chart 1, it looks like there is a very clear positive relationship between the mean returns and its momentum return decile. Each decile has a higher mean return than its previous decile. Similarly, there is a very clear positive relationship between a stock’s return decile and its standard deviation. Every decile has a lower standard deviation than its previous decile.

Chart 1

Chart 2

This was reasonable because it would suggest that investors can gain more rewards for taking more risks. However, when we use the annualized standard deviation calculated by monthly data, the lower decile has a higher annualized standard deviation.We guessed that there might be a small probability of a very catastrophic reversion to the mean, which makes higher decile stocks riskier and underperforming stocks less risky.

Consequently, we calculated the skew and kurtosis for the distribution of returns for each decile, as shown in charts 3 and 4, and our findings supported our initial guess when we used monthly return data, which we believe can generate a more accurate distribution.

Higher decile stocks had a negative skew. This meant fatter tails for them in the distribution, which made them riskier when the market crashed. However, the higher decile portfolios have…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.