American Home Products Corp. - Case Solution

American Home Products Corp. case study allows students to look into a virtually no-debt company and its debt policy. It seeks to identify if acquiring some debt may be valuable for some shareholders and the company, as a whole.

Case questions answered:

- Analyze each of the four different capital structures shown in Exhibit 3, plus the capital structure that would result if the only thing American Home Products Corp. does is to use $233 million to repurchase shares. In particular, for each capital structure, calculate the leverage ratio based on market values (can use book value of existing debt), number of repurchased shares, price per share, interest coverage (EBIT/interest), EPS, and the P/E ratio (use after-tax earnings for last two measures). Do you see any trends in the price per share, interest coverage, EPS, and P/E? Explain these trends. For this question, assume that the interest tax shield has zero value (that is, assume that the value of AHP does not increase with increased leverage).

- Now, suppose that the tax shield generated by the debt has its maximum value (Tc = 48%). Suppose that shares can be repurchased for $30 per share. Repeat the exercise from Question 1. Explain your valuation of the tax shield.

- Calculate the percentage increase in price per share under the different scenarios in Question 2 compared to the benchmark price of doing nothing ($30). For each scenario, compare this percentage increase in price per (non-repurchased) share to the percentage increase in value to all shareholders created by the tax shield of the debt. You will see that the latter is smaller. Why?

- Repeat Question 2, but now assume that shares are repurchased at their fair market price.

- Repeat Question 2, assuming that shares are repurchased at their fair market price and that the maturity of any new debt is 10 years. After this period, American Home Products will not renew the debt.

- Which capital structure would you recommend and why? (You need to think about the expected bankruptcy costs in the different scenarios. Think about how likely bankruptcy would be in different scenarios.) Please also comment on any other relevant considerations beyond bankruptcy and taxes for your recommendation.

American Home Products Corp. Case Answers

![]() This case solution includes an Excel file with calculations.

This case solution includes an Excel file with calculations.

Executive Summary - American Home Products Corp.

American Home Products Corp. (AHP) has been one of the leading brands in the field of prescription drugs, food items, packaged goods, and household products. The company’s most profitable unit is prescription drugs, which have a well-diversified and sizeable market share. The firm’s CEO has been a very strong advocate of a debt-free capital structure and has believed in running the firm through internal financing.

For the past decade or so, we have seen the firm being able to perform well under his leadership and management. The firm’s increasing revenues and cash reserves are a testament to it, which is why the CEO’s opinion hasn’t changed. AHP has had enough cash flow (28.2% of total assets in 1981) to cover its operating costs. The firm’s risk aversion culture has to lead the company’s preference to acquire or buy licenses of existing products rather than invest in developing new products with better technology.

With the current CEO’s term coming to an end, we believe this is the perfect opportunity to look into the option of change in the capital structure strategy American Home Products has been operating with. The current debt is almost negligible. We have tested out some scenarios in which the firm undertakes debt to repurchase shares and the consequences it will have on the firm’s profitability and stock market performance. We have tested three different debt-to-capital structures (30%, 50%, and 70% debt) and used the additional cash to repurchase shares. We have looked into our peer Warner-Lambert and have kept $360.3 million, which we believe is necessary to finance operations.

The analysis across different capital structures incorporating various assumptions reveals that the inclusion of debt leads to multiple benefits to the firm’s market presence. A moderate leverage structure incorporating 30% debt is the most appropriate capital structure, which would enable the repurchase of more than 19 million common shares outstanding using the debt undertaken and excess cash reserves. This would increase earnings per share (EPS) and the dividends paid out as the payout ratio would remain constant.

The other advantage would be the tax savings of $39.8 million, which would also benefit our shareholders. Other important financial indicators used by a financial analyst in the market, such as return on equity (RoE) and return on capital employed (RoC), also increase, which would also send out a positive signal to the market. The earnings can cover the interest expense outlay easily, and the firm would even have the option to take more debt in the future if there’s a need without the worry of higher credit spreads.

The firm’s peer, Warner-Lambert, has also adopted a capital structure similar to our recommendations of 30% debt, and given the credit ratings of AAA/AA for Warner-Lambert, American Home Products will not face any downgrading risk on its credit ratings. With a similar capital structure in place and strong earnings projections, AHP will also be able to secure the highest possible rating. There are negligible bankruptcy or distress costs in this scenario.

We, therefore, recommend an aggressive capital structure instead of a conservative low-risk strategy; this would mean the use of more debt in the company’s operations. A higher degree of innovation and research is required to be more effective in the market. Meaningful differentiation can only be possible through constantly developing solutions that meet the unarticulated needs of the market. Among the three debt structures analyzed, 30% debt seems to be the most appropriate choice for management.

American Home Products has been a household name that has operated in many different sectors. Their business has been distributed among prescribed drugs, food items, household products, and packaged medication. The business risk of AHP can be deemed on the lower side of the spectrum, considering the business lines of the firm.

The firm’s operational activities have not been leveraged, and thus, the amount of business risk involved is at a significantly lower level compared to its peers. The firm managed its business operations with its accumulated cash reserves with an almost negligible risk of default.

The case wanted us to analyze the prospect of changes to basic financial ratios and valuations by introducing different levels of debt. The results clearly suggest that even though the business risk positively correlates with the increase in the firm’s leverage, there is a very significant increase in the returns of the shareholders, which, according to the firm’s CEO, has always been the priority.

We see that when the debt ratio of the firm increases from 0.93% to 30%, the return on equity appreciates from 33.6% to 51.5%. As we go further with higher levels of debt, like 50% and 70%, the return on equity comes out to be 69.2% and 110.5%, respectively. So, the shareholders would eventually benefit from the capital restructuring depending upon the risk appetite of the management of American Home Products.

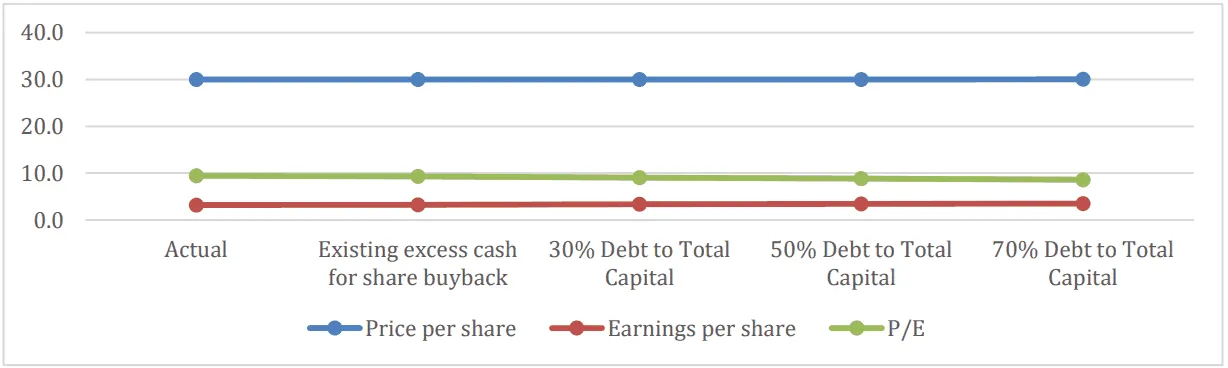

Under the given assumption of no tax shield, the price per share after restructuring doesn’t change. Even though the market value of equity reduces with the increase in the debt, the number of shares outstanding also decreases in an equal proportion. Thus, the share price stays at $30 for all the different capital structures. This is also in agreement with the first Modigliani and Miller proposition of capital structure irrelevance to the firm value and hence stock price.

Capital restructuring from no debt to higher debt ratios leads us to depreciate P/E ratios. The P/E ratio reduces from 9.4 to 9.0 when the leverage in the capital structure is increased from 0.93% to 30%, which means a lower price to be paid per unit of earnings. Also, there is a positive correlation between the EPS and the leverage of American Home Products. So, the stakeholders get higher earnings per share with capital restructuring (Appendix 1).

The interest coverage at less than 1% leverage is significantly high (415.1), indicating the possible benefits of corporate restructuring. At higher debt ratios of 30%, 50%, and 70%, the value of interest coverage falls to 17.5, 10.5, and 7.5, respectively. The high earnings allow the firm freedom to afford an increase in debt percentage and thus the business risk in order to maximize the returns.

The trend in share price, EPS, and P/E if there are no tax shields

We also analyze the case considering the inclusion of the tax shield advantage that American Home Products would benefit from when they restructure and add debt, and we measure those effects on the shareholders. With the added tax benefits, the market value of the equity increases, thereby increasing the price per share.We assume that the information related to added tax benefits does not get reflected in the stock price before the purchase, and the buyback happens at $30 per share at all levels of debt. The added tax benefits are distributed among the investors who prefer to stay with the firm. Also, there is a positive correlation between the level of debt undertaken and the new share price after the exchange.

The earnings per share don’t get affected by the tax shield, but…

Unlock Case Solution Now!

Get instant access to this case solution with a simple, one-time payment ($24.90).

After purchase:

- Solution files delivered straight to your inbox.

- Secure checkout — no account required.

Best decision to get my homework done faster!

Michael

MBA student, Boston

FAQ

How do I get access?

Upon purchase, you are forwarded to the full solution and also receive access via email.

Is it safe to pay?

Yes! We use secure payment providers to process your transaction safely.

What is Casehero?

We are the marketplace for case solutions - created by students, for students.